/ua-templates/version3/images/swbanner/swlogo-hz.png)

Health Care Costs Could Have Significant Impact on the Future: Part One

Article Four in the Series on Health Care

by Rachel Voris

A few years ago when I was going through the awkward transition from college to my first career job, I remember complaining to a friend, five years my senior, about feeling lost in deciding what health plan to choose with my new job.

My friend, a very honest, black and white thinker, told me about a high deductible health plan tied to a health savings account. It sounded too good to be true—a plan with the lowest out of pocket expense that allowed me to save untaxed money to use for my health expenses.

The University of Alaska is exploring offering a plan just like that, in part driving employees towards a consumer-driven health care approach to better align with a new era of ever-rising medical costs and inflation. Many factors go into determining which plans are right for UA employees including a close look at projections, fiscal year activity, actual cost of health care from year to year and how much those numbers affect employee rates. In talking about these subjects, it is important to know some key vocabulary terms identified here:

Vocabulary terms:

- Over recovery: the amount paid by employees is more than costs needed to be recovered.

- Under recovery: the amount paid by employees is less than costs needed to be recovered.

- Actual cost: the cost that occurs during a fiscal year.

- Projected cost: the estimate of cost for health care during a fiscal year.

- Fiscal year: The fiscal calendar year begins on July 1 and runs through June 30 every year.

Determining the Cost of Health Care Annually

An annual accounting cycle takes place to determine the rates for UA Choice health plans. Estimates of health care costs are made each fiscal year, which occurs from July 1 through June 30. After the fiscal year ends in July, the Statewide Payroll and Benefit Accounting Office determines the actual cost and recoveries for the prior year. If estimates are higher or lower than actual cost, the university will either have to recover money or the university has a surplus to offset future costs. The actual cost and recovery amount is important because it impacts rates that employees may pay in future periods.

Over and under recovery has had an effect on UA plans in recent years. Fiscal year (FY) 12 was an under recovery year, and the university had to make a plan to recover $2.8 million in lost funds the following fiscal year. There are many reasons behind this significant under recovery amount in FY 12.

Beginning in July 2011, a new high deductible health plan (HDHP) was offered. UA also has a 500 plan (click here for Employee Handbook with plan details) and a 750 plan. Many more employees migrated toward the new plan than originally estimated, according to Michelle Pope , director of Payroll and Benefit Accounting Department. The movement to the new plan was good overall since it lowered the plan cost, but the university was not able to recover as much from employees through biweekly deductions since the high deductible plan has the lowest payroll deduction of the three plans offered. Employees enrolled in the 500 plan pay higher payroll deductions than employees enrolled in the high deductible plan. Many employees moved from higher benefit plans to the lower benefit plans and the rates were not calculated to accommodate a move of that size. As a result the university did not recover as much as needed, Pope explained.�

The under recovery was compounded further because the FY 12 employee rates were kept the same as the FY 11 rates, which were artificially low because of a prior over recovery, explained Director of Benefits at the Statewide Benefits Office Erika Van Flein. When the rates were set and kept the same for the next year, the Joint Health Care Committee (JHCC) understood that there would be an under recovery. The JHCC decided it would be better to have an under recovery than impose a new plan option and cost increase in the same year.

An under recovery of $500,000 was also expected because a tobacco surcharge (click here for information on surcharge) was built into the plan, even though it was never implemented. “The rates were already set by the time it was decided not to implement the surcharge,” Pope said. “It was too late in the process to change anything.”

Because the UA didn't implement a tobacco surcharge and kept the rates at the FY 11 level, a total under recovery of $1.5 million was projected for FY 12. When the FY 13 rates were set, there was a total under recovery estimated to be about $3.5 million due to additional under recovery of nearly $2 million because of the migration to the higher deductible plans. Rates were subsequently increased for FY 13 to recapture some of that cost, following a lengthy process where the JHCC viewed many different hypothetical collection scenarios with different projections for collections in different years. The JHCC reviewed the scenarios and voted to do 80 percent of the recovery, $2.9 million, in FY 13 and the other 20 percent in future years.

“This is exactly what we look to the JHCC for,” Van Flein said. “If we are going to have to increase rates, and we have reasons behind it, the JHCC helps to guide how those rates are presented to employees.” For information about the JHCC and their role within UA Health Care, go here.

This solution still wasn’t ideal though. In FY 14, the university contribution towards health plans will change from 83 percent to 82 percent, which will mean a one percent rate increase on employees.

The Importance of Actuals

The university was facing a dilemma: increases due to under recovery combined with increases due to the changes in contribution.

“If we were to extend that under recovery to a future time, we would have an under recovery increase and another one percent increase of rates based on the change in university contribution. It’s best to recover as much as you can in one year, especially in an under recovery situation so that employees down the road don’t have to deal with recovery,” Pope said.

The solution came during the time (August to October) when the actual cost of care is compared to the projected cost. “In February, we were dealing with projections. We were guessing what the cost would be for the rest of the year and what was going to happen. Now that time has passed, we are looking at what we are actually getting in cost and what is actually being recovered from employees,” Pope said.

The actual under recovery for FY12 ended up being only $2.8 million. The university is projected to recapture the entire cost of under recovery in FY 13. “The great news is that we shouldn’t have any FY 13 under recovery rolling over into FY 14 as long as FY 13 projections are in line with FY 13 actual costs,” Pope said.

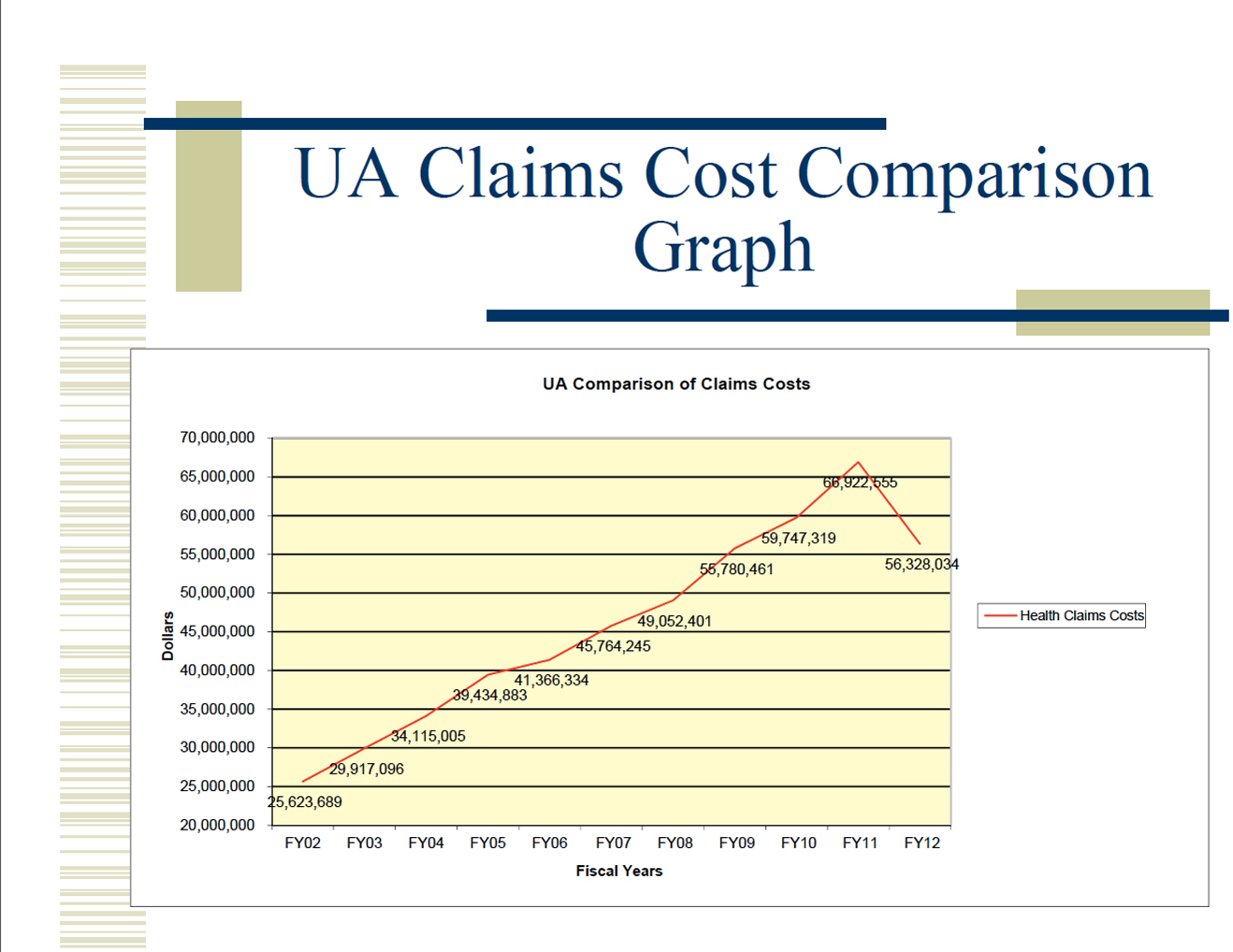

After the actuals are compared to projected figures, the university and the JHCC begin to look at possible health plan design changes to deal with overall rising costs. Adding the high deductible plan did lower overall claims in FY 12 by about $6 million, but that cost reduction was a one-time experience due to plan design change. Typically, there is an increase from eight to 10 percent in cost every year. “Health care costs continue to increase. It’s just that this year we had one year in which employees were covering more of the up front cost because of the plan design change. Now that the plan design is what it is, we expect to begin experiencing the normal increase,” Pope explained.

“Just because we changed our plan doesn’t mean that health care inflation went away,” Van Flein said.

Conclusion: The Bigger Picture

The numbers play a large roll in determining plan design for employees. The UA is trying to offer the best plan at the lowest price. In order to do this, the UA and the JHCC are looking at making plan design changes to make way for a high deductible plan used in conjunction with a health savings account.

Next month, part two of this article will cover the recent motions made by the JHCC including suggested plan design changes to help with the overall notion of consumerism—the way the employee uses health care. The considerations include a review of the impact of the health care task force report, found here (HCTF Final Report ), which looked at ways to raise awareness about health in the UA community as well as ideas for improving the use of preventative care and wellness benefits.

/ua-templates/version3/images/swLogo.gif)